Unbeknownst to many in the wine trade, a quiet revolution has taken place following the 2008 GFC. Many smaller wine businesses have completely reinvented their business models targeting direct to consumer sales.

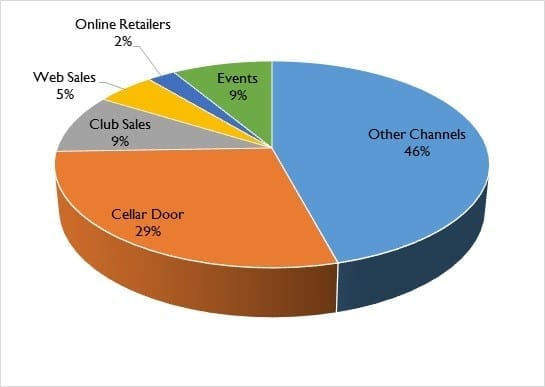

In a new report released this week – Taking the Direct Route 2014 – we revealed that wineries in Australia, New Zealand and South Africa who produce less than 50,000 cases now sell more than 50% of their wine Direct to Consumer. All aspects of Direct sales – Cellar Door (+8%), Club Sales (+23%), Web Sales (+14%) and Events (+7%), grew strongly year on year.

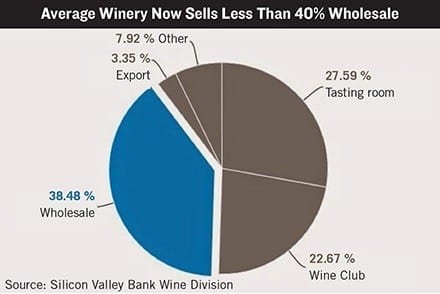

This mirrors research by Silicon Valley bank (also released this week) that shows that the average US winery producing less than 10,000 cases sells more than half of its wine Direct to Consumer as well.

According to Silicon Valley Bank’s Rob McMillan “Wholesalers don’t want small wineries. Distribution isn’t available for most wineries, so they have had to elect more Direct to Consumer options.”

The factors driving change in Australia, South Africa and New Zealand are more numerous and more intensive than in the US. US producers were at least blest with a booming local market during the post GFC period.

Strong currency has been a major issue to Australian and New Zealand producers. Australia has major problems with its brand in the US and is struggling in Europe as well. South Africa has had a good run with its currency and bulk producers have done well recently. Smaller South African producers understand the limits of their home market, however, and have become much more sophisticated at working inbound wine tourism markets in order to sell directly to an international audience. Australian and New Zealand producers need to do the same.

Whilst UK importers generally have a very different attitude to working with smaller wineries than most US distributors, (proximity to Burgundy has a lot to do with that) the fact that UK grocers have made it almost impossible for any winery to sell profitably is another factor driving smaller producers to seek more sustainable sales.

Australian retail concentration led by supermarkets has also had a huge impact on smaller Australia and New Zealand producers (although some smaller New Zealand producers a still coming to grips with their lack of suitability for this channel).

When you add to that the increased control over all aspects of brand building that you get with direct sales, it becomes compelling.

The only down side I see is that through falling out of global distribution, regional and country brand reputations will suffer. This may not matter to US producers but it matters hugely to Southern Hemisphere countries who typically export more than half of their wine.

It is still vitally important, for Australian producers particularly, to be talking to sommeliers in London, New York and Tokyo about the outstanding quality of wines being produced by young winemakers as this is where the trends get set for the regions in major markets like the UK, for China and other developing markets and for the wine world more broadly.”

Purchase a copy of the Taking the Direct Route 2014 report.

Or for more information, send me an email [email protected]