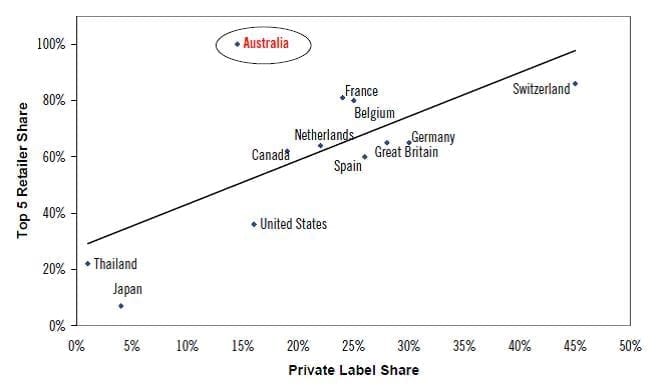

In mid-2007, Citigroup’s Andy Bowley correctly identified that Australia was absolutely ripe for expansion of own label.

No other major market on earth (with the possible exception of Portugal and New Zealand not shown of this chart) has such concentration of buying power amongst its leading supermarkets. At the same time, the penetration of private label in the packaged alcoholic beverage category was much lower than in most other markets.

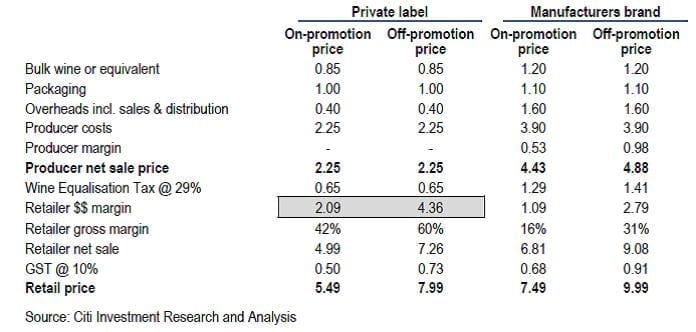

{kind=link}

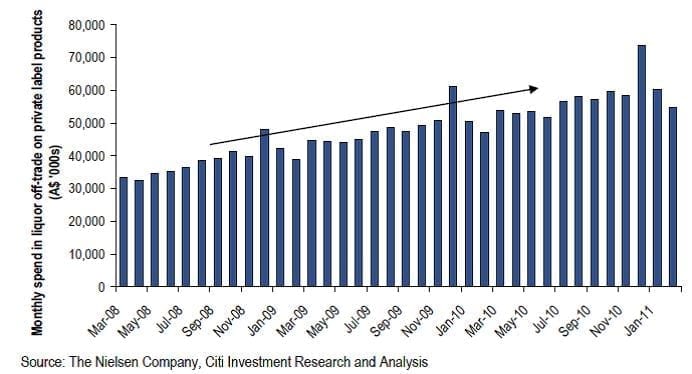

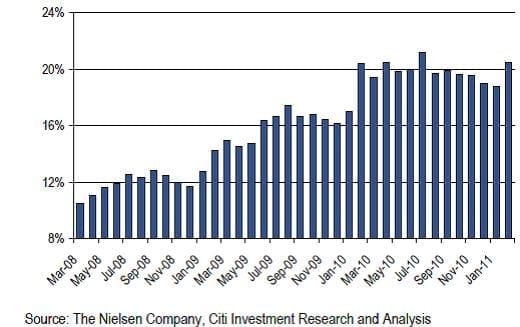

From that point forward, private label rapidly increased its share of packaged alcohol. 20% of Off-Trade sales were private label by April 2011.

Where wine is concerned, however, private label penetration seems to have plateaued as at around that 20% figure.

This is an almost identical situation to the UK where, after dipping to as low as 18.7% in 2009, Private label pushed back up over 20% again in 2010 in response to the GFC.

This is a vastly different number to those which are so often lauded over perspective suppliers to Tesco, Sainsburys and Mark & Spencer and the like.

Whilst some chains have claimed as high as 60% of sales as own label in the past, one 5th of sales seems to be the natural equilibrium.

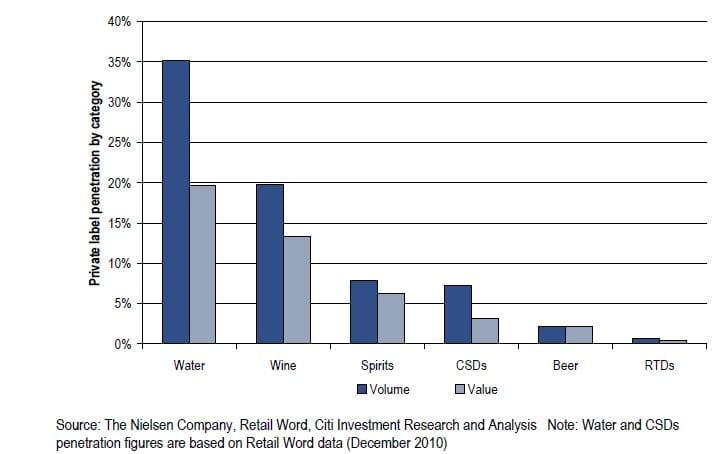

The US, led by Costco, is moving toward that same level. As discussed in the Wine Paper 18, private label is out performing many of the major companies but not the mass of other smaller competitors.

Why is this so? The market is rapidly “premiumising”, smaller players are much better competitors than large at premium price points and consumers of these wines do not want private labels.

They want to know that their wines were made by “real” people from a “real” place. The chart below substantiates this.

{kind=link}

Supermarkets will aggressively push for more private labels because they make more money.

What must medium sized companies do? Are “Gear Up” or “Get Out” the only choices?

“Gear Up” – develop competitive scale and supply chain efficiencies so as to become a cost competitive supplier. Warburn Estate has chosen this model. They now have one customer – Woolworths. Whilst there are some considerable risks associated with this approach, their growth has been nothing short of phenomenal. Their imports of NZ wine alone amount to nearly 1 million cases. Their situation now is not unlike suppliers of potatoes to McDonlads.

“Get Out” meaning; –

- Forgetting about selling wine below $15 per bottle retail

- Focusing on leading regions as the source of fruit

- Developing brands with strong regionally based identities and distinctive personalities.

There are, of course, other options. WBS client Beelgara made over $2million in EBITDA last year pursuing an innovative multichannel approach. Grant Burge is another WBS client who has been highly successful through using innovation to evolve their business to best take advantage of the new paradigm.

Perhaps the current drive to “break up the supermarkets” in Australia will succeed. Probably it will not. The argument is, in my view, yet another distraction full of politicking and misinformation that, for smaller producers, has practically no relevance. Medium sized producers need to be evolving their competitive strategy rapidly both as good discipline and in any case.